Quick Answer

Mortgage underwriting in Florida is the stage where your income, assets, credit, employment, and property details are reviewed before final loan approval. During this process, underwriters verify financial information, request any needed documentation, and confirm that the loan meets all approval requirements before closing.

Top 3 Take-a-Ways

- Additional document requests are usually a normal part of underwriting

- Financial changes during underwriting can delay or jeopardize approval

- Fast responses help keep loans moving toward closing

Buying a home can feel exciting right up until the word “underwriting” comes up. For many buyers, that’s the point where stress kicks in. Suddenly there are document requests, questions about bank statements, and worries about whether the loan will actually get approved.

That’s why it helps to understand mortgage underwriting in Florida before you get there. Once you know what underwriters review and why they ask for documents, the process usually feels much less intimidating.

Alex’s Professional Insights

Over the years, I’ve noticed that mortgage underwriting in Florida causes more anxiety than almost any other part of the home buying process. I remember working with a buyer who became convinced their loan was going to be denied because the underwriter kept requesting additional documents. They called me several times worrying that every new request meant something was wrong. In reality, the requests were routine verification items, and the loan closed on schedule without any issues.

Experiences like that have taught me that underwriting is often less about finding problems and more about confirming details. The buyers who have the smoothest experience are usually the ones who stay organized, respond quickly, and avoid making major financial changes during the process. Understanding what underwriting is designed to accomplish can remove a lot of unnecessary stress and help buyers feel much more confident from application to closing.

What Is Mortgage Underwriting In Florida?

Mortgage underwriting is the process where your financial information gets reviewed to make sure you qualify for a home loan. Think of it as the stage where your application moves from “initial review” to “final verification.”

During underwriting, financial details are reviewed to confirm things like:

- Income stability

- Employment history

- Credit profile

- Monthly debt obligations

- Savings and assets

- Property value

- Insurance requirements

The goal is simple. Underwriting is designed to confirm that buyers can reasonably afford the mortgage based on documented financial information.

Many buyers assume pre approval means everything is finished, but underwriting is where the deeper review happens. Pre approval is often based on an early review of documents, while mortgage underwriting in Florida usually includes more detailed verification before final approval.

The timeline can vary depending on the type of loan, property, and how quickly documents are submitted. According to recent 2026 mortgage processing data, the average time to close a purchase mortgage typically ranges around 40 to 50 days nationwide, though some Florida purchases move faster when documents are organized early.

Condo purchases, self employed borrowers, investment properties, and jumbo loans may sometimes take longer because additional documentation is often required.

What Documents Do Underwriters Review?

This is where many buyers get surprised.

Mortgage underwriting in Florida usually involves more paperwork than people expect. Underwriters aren’t trying to make things difficult. Their job is simply to confirm the information already provided in the application.

Common documents often include:

- Recent pay stubs

- W-2 forms

- Tax returns

- Bank statements

- Retirement account statements

- Investment account balances

- Driver’s license or identification

- Employment verification

- Homeowners insurance information

For self employed buyers, additional documents are often needed. Profit and loss statements, business bank statements, and multiple years of tax returns may become part of the review.

Large deposits in bank accounts often receive extra attention too. If someone deposits $15,000 into an account right before closing, underwriting may ask where it came from. That doesn’t mean something is wrong. It usually just means the money needs documentation.

Income structure can also affect underwriting. Hourly income, salary, bonuses, commissions, overtime, and self employment earnings may all be reviewed differently.

Credit matters too, but not always the way buyers think. A single late payment doesn’t automatically stop approval. Instead, underwriters often look at the overall financial picture, including debt levels, payment history, and cash reserves.

Debt to income ratio also becomes important. This compares monthly debt payments to monthly income. If you’d like to get a clearer picture of affordability before applying, you can compare different payment scenarios using our Mortgage Calculator.

Why Do Underwriters Ask For More Documents?

This is probably the biggest source of stress during mortgage underwriting in Florida.

A buyer uploads documents, thinks everything is complete, and then suddenly gets asked for more paperwork. Many people assume that means something went wrong.

Most of the time, it doesn’t.

Additional requests are often called “conditions.” These are simply follow up items needed to finish the file.

Some common reasons underwriters request more documents include:

- Clarifying large bank deposits

- Verifying recent employment changes

- Updating expired pay stubs or bank statements

- Confirming debts on a credit report

- Explaining credit inquiries

- Verifying source of down payment funds

For example, someone may transfer money between accounts and underwriting simply wants confirmation showing both sides of the transfer. Or an underwriter may request a letter explaining a temporary job gap.

Employment consistency and financial stability can play a major role in mortgage underwriting in Florida, especially when buyers have variable income, bonuses, or self employment earnings. Stable employment history and documented income often help files move more smoothly through the process.

The important thing to remember is that requests for documents are normal. In many cases, a file receiving conditions means underwriting is actively moving forward, not falling apart.

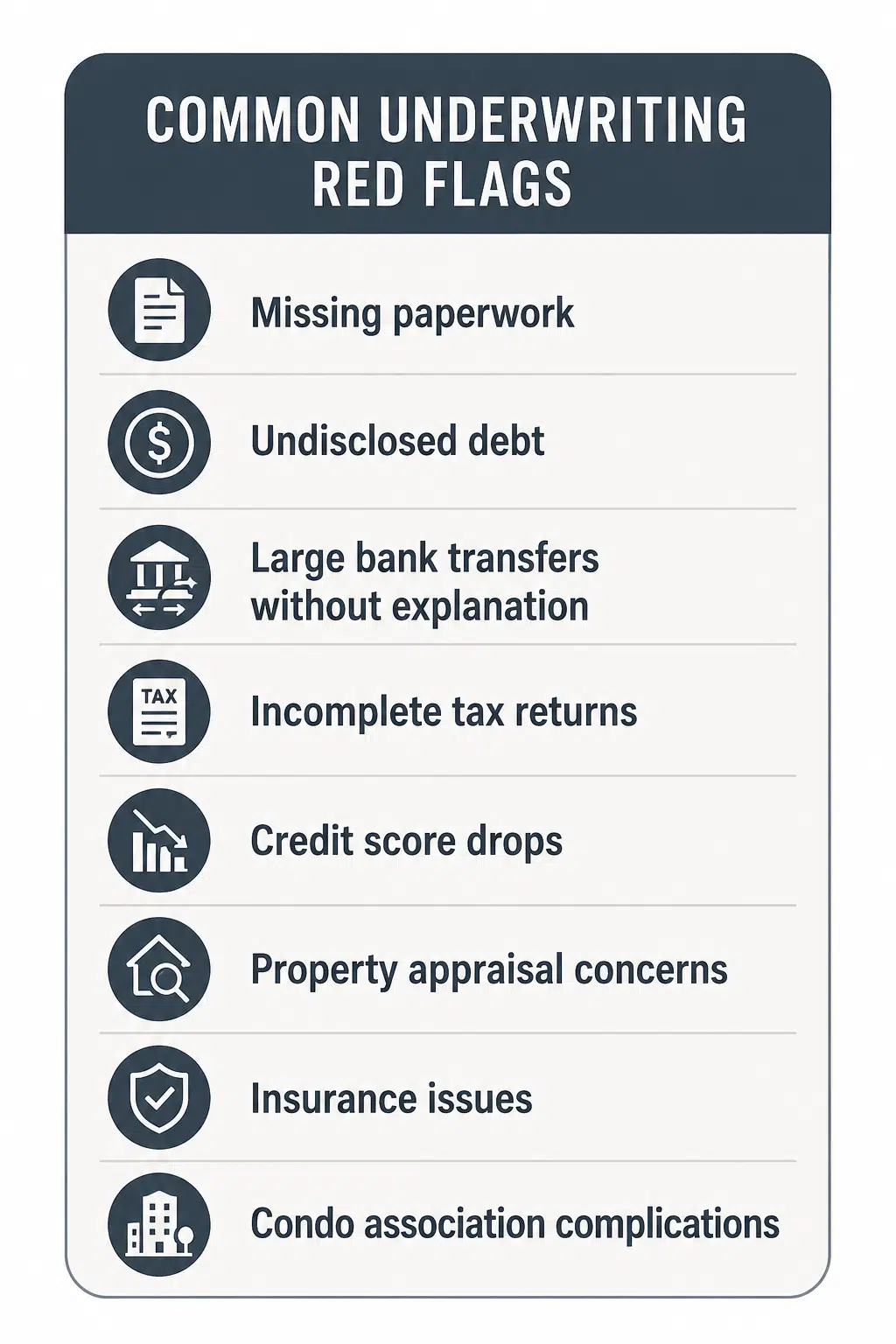

What Red Flags Can Delay Mortgage Underwriting?

Most buyers hope mortgage underwriting in Florida will move quickly, but certain issues can slow things down if they aren’t handled early.

The good news is that many underwriting delays are avoidable.

One of the biggest problems is large unexplained deposits. If a buyer suddenly deposits $10,000 or $20,000 into a bank account without documentation, underwriting may pause while additional verification is requested. This doesn’t automatically mean there’s a problem. It simply means the money needs to be sourced.

Job changes can also create delays.

Switching employers, moving from salary to commission income, or becoming self employed during underwriting may require extra review. Stability matters during mortgage underwriting in Florida, which is why many buyers wait until after closing before making career changes.

New debt is another common issue.

Opening a credit card, financing furniture, or buying a car before closing can change debt to income ratios quickly. Something that looked affordable at the beginning of underwriting may suddenly require additional review after new monthly payments appear.

Appraisals can create delays too.

If a home appraises lower than expected, the transaction may need to be renegotiated or restructured. Condo purchases sometimes take longer because additional building documents may need review, especially in Florida communities with reserve requirements or insurance concerns.

Insurance can also affect timing. In Florida, homeowners insurance and flood insurance sometimes take longer to finalize than buyers expect, especially for waterfront or older properties.

According to recent 2026 mortgage approval data, loans with incomplete documentation and unresolved financial questions are among the most common reasons for processing delays.

The easiest way to avoid most underwriting issues is staying financially stable during the process. Avoid major purchases, don’t open new credit, and respond quickly when documents are requested.

How Long Does Mortgage Underwriting In Florida Take?

One of the most common questions buyers ask is how long underwriting actually lasts.

The honest answer is that it depends.

Some files move through mortgage underwriting in Florida in just a few days, while others take several weeks depending on complexity.

In many standard purchase transactions, underwriting may take anywhere from several business days to two weeks once the file reaches a full review stage. However, overall closing timelines often stretch longer because underwriting requests, appraisal timing, title work, insurance, and final approval still need completion.

Several things can affect timing, including:

- Type of loan

- Self employed income

- Condo purchases

- Jumbo financing

- Appraisal complexity

- Insurance review

- Speed of document submission

- Property type

For example, a buyer with straightforward W-2 income purchasing a single family home may move through underwriting faster than someone purchasing a waterfront condo with self employment income and multiple bank accounts.

Mortgage underwriting in Florida may also take longer during busy home buying seasons when loan volume increases.

Florida condos sometimes create extra steps because HOA budgets, reserve studies, insurance documents, and occupancy details may require review. Buyers purchasing second homes or investment properties may also experience more conditions compared with primary residence purchases.

This is one reason preparation matters so much. Organized buyers who submit requested documents quickly often experience smoother underwriting timelines.

Can You Be Denied During Underwriting?

Yes, but it’s not as common as many buyers fear.

Most buyers who reach underwriting and remain financially consistent ultimately make it to closing. Problems usually happen when financial situations change during the process or major documentation issues appear.

Some of the most common reasons buyers run into problems during mortgage underwriting in Florida include:

- New debt during underwriting

- Job loss or employment changes

- Missing financial documents

- Large undocumented deposits

- Credit score drops

- Property issues

- Appraisal shortfalls

- Undisclosed obligations

For example, buying a vehicle before closing may increase monthly debt enough to change qualification. Moving large amounts of money without documentation can also create questions that delay approval.

Employment and income stability play an especially important role. Income consistency, debt levels, and financial documentation can all influence mortgage approval in Florida, particularly for self employed borrowers or buyers with variable income.

The best way to reduce risk is keeping everything stable until closing. Don’t make large purchases, avoid moving money unnecessarily, and respond quickly when underwriting asks for updates.

If you’d like a clearer idea of what your numbers may look like before underwriting begins, you can request a free, instant quote.

What Can You Do To Help Underwriting Go Smoothly?

The good news about mortgage underwriting in Florida is that buyers often have more control over the process than they realize.

The smoother the file, the faster underwriting usually moves. Most delays happen because of missing paperwork, financial changes, or slow responses to document requests.

A few simple habits can help underwriting move much more smoothly:

- Respond quickly to document requests

- Avoid opening new credit accounts

- Don’t finance furniture or cars before closing

- Keep income and employment stable

- Avoid moving large amounts of money unnecessarily

- Keep bank account activity easy to explain

- Stay in communication throughout the process

One of the smartest things buyers can do is avoid major financial changes until after closing. Even small decisions can sometimes create unexpected delays.

For example, financing a new appliance package, co-signing a loan for someone, or opening a new credit card may affect debt to income calculations. Something that looked fully approved a week earlier may suddenly require additional review.

Mortgage underwriting in Florida also tends to move faster when buyers submit documents early and completely. If underwriting asks for updated bank statements, insurance information, or verification documents, responding quickly can help keep timelines on track.

Florida buyers purchasing condos, waterfront homes, or second homes may also experience more requests because of insurance and property specific review. Flood insurance, HOA reserves, and condo documentation can sometimes add extra steps during underwriting.

According to recent 2026 mortgage processing research, documentation delays remain one of the biggest reasons mortgage approvals take longer than expected.

Affordability preparation matters too. Buyers comparing different payment options before applying often feel more confident once underwriting begins. Different loan structures, taxes, insurance costs, and down payment options can create very different monthly payments.

FAQ’s

How long does mortgage underwriting in Florida take?

Many files move through underwriting in several business days to two weeks, though total closing timelines often depend on appraisals, insurance, and document requests.

Can underwriting deny a mortgage after pre approval?

Yes, but most buyers who stay financially stable and provide documentation successfully move forward.

Why do underwriters ask for so many documents?

Underwriters verify income, assets, debts, employment, and financial stability before final approval.

Can I buy a car during underwriting?

It’s usually best to wait. A new car payment may change debt to income ratios and affect approval.

What happens after underwriting approval?

Once underwriting signs off and remaining conditions are cleared, the loan typically moves toward final closing.

Do self employed buyers face stricter underwriting?

Often, yes. Business owners may need extra tax returns, bank statements, and profit documentation.

Why We Help Buyers Feel More Prepared

We understand that mortgage underwriting in Florida can feel stressful, especially when buyers start receiving document requests and unexpected questions. Most people worry something is wrong when underwriting asks for more information, even though those requests are often completely normal.

Our team works closely with buyers throughout underwriting so they understand what’s happening and what to expect next. We help review income, assets, documentation, conditions, and timelines before problems become bigger issues.

We’re proud that The Doce Mortgage Group was recently recognized by WalletHub as one of the best mortgage brokers in several Florida cities. Many buyers also read through customer reviews before deciding who they want helping them through one of the biggest financial decisions of their lives.

Our goal is to help buyers feel informed and confident throughout mortgage underwriting in Florida so the process feels less stressful and more predictable from start to finish.

When you’re ready to move forward with financing, you can get started now, or connect with a loan officer live at 305-661-3434.