Quick Answer

Mortgage discount points let Florida homebuyers pay an upfront fee at closing to secure a lower interest rate. This lowers the monthly payment and can save money over time if you keep the mortgage long enough.

Table of Contents

- Why Do Mortgage Discount Points Exist?

- How Mortgage Discount Points Affect Your Interest Rate

- How Much Does One Mortgage Discount Point Cost In Florida In 2025?

- Why Point Costs Feel Higher For Florida Buyers

- Can You Buy Partial Points Or Multiple Points?

- How Point Costs Interact With Other Closing Expenses

- How Much Can Mortgage Discount Points Lower Your Interest Rate In 2025?

- Why Interest Rate Reductions Are Not Fixed

- Why Florida Buyers Often See Strong Value From Points

- Comparing Rate Options Before You Decide

- What Is The Break Even Point When Buying Mortgage Discount Points?

- Why Break Even Timing Matters For Florida Buyers

- How To Estimate Your Break Even Point Accurately

- Can Seller Credits Be Used To Pay For Mortgage Discount Points In Florida?

- Do Mortgage Discount Points Work The Same Across All Loan Types?

- Should You Buy Mortgage Discount Points If You Plan To Refinance?

- Can Mortgage Discount Points Be Tax Deductible?

- Common Misunderstandings About Mortgage Discount Points

- FAQ’s

- How We Help Florida Buyers Decide If Discount Points Make Sense

Top 3 Take-a-Ways

- Points make sense only if you keep the mortgage past the break even point.

- Higher Florida loan amounts increase both point costs and potential savings.

- Seller credits can sometimes cover points without increasing cash to close.

Why Do Mortgage Discount Points Exist?

Mortgage discount points are an optional upfront cost that Florida homebuyers can choose to pay at closing in exchange for a lower interest rate on their mortgage. When you buy discount points, you are paying part of the interest ahead of time so your monthly payment is lower for as long as you keep the loan.

Each discount point equals one percent of the total loan amount. On a $400,000 mortgage, one discount point would cost $4,000. This amount is paid at closing and is separate from your down payment and other standard closing expenses.

Discount points are optional. You are never required to buy them. Instead, they are offered as part of your interest rate choices so you can decide how to balance upfront costs with long term monthly savings.

Why Do Mortgage Discount Points Exist?

Here are a few key reasons discount points exist:

• To give buyers control over loan pricing

• To reduce monthly payments over time

• To offer an alternative to accepting a higher interest rate

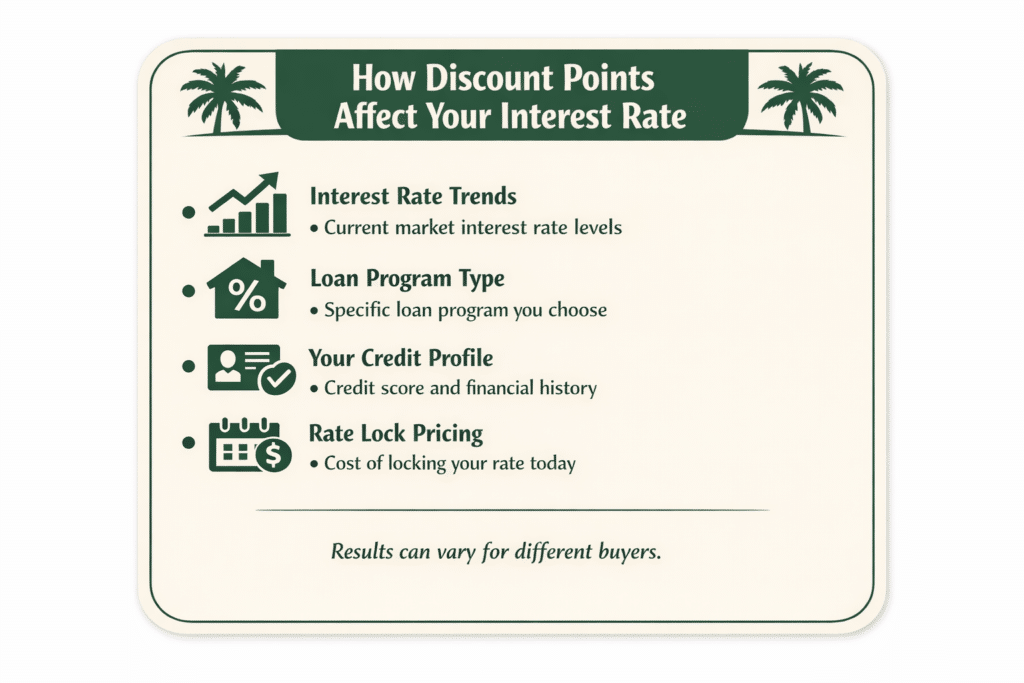

How Mortgage Discount Points Affect Your Interest Rate

Several factors influence how much your rate is reduced when you buy points:

• Overall interest rate environment

• Loan program type

• Credit profile

• Market pricing on the day of rate lock

Because of these variables, two buyers paying the same number of points may see slightly different results.

If you want to see how points could affect your payment in real numbers, run a couple side by side scenarios using the Mortgage Calculator.

How Much Does One Mortgage Discount Point Cost In Florida In 2025?

Here is how the math works using common Florida price ranges:

• A $300,000 mortgage equals $3,000 per point

• A $400,000 mortgage equals $4,000 per point

• A $500,000 mortgage equals $5,000 per point

Because points are calculated as a percentage, higher loan amounts increase the cost quickly. This is why understanding your exact loan size is critical before deciding whether points make sense.

Why Point Costs Feel Higher For Florida Buyers

Florida buyers often feel the impact of discount point pricing more than buyers in lower cost states. That is not because points are priced differently here, but because property values and loan balances tend to be larger.

Florida Realtors data shows that median prices in metro areas like Miami, Fort Lauderdale, Tampa, and Orlando remain well above national averages. When loan amounts rise, point costs rise with them, even though the percentage stays the same.

This is why buyers should always look at both sides of the equation:

• The upfront cost of the points

• The monthly savings created by the lower rate

Looking at only one side can lead to a decision that does not align with your long term plans.

Can You Buy Partial Points Or Multiple Points?

Yes, discount points do not have to be purchased in whole numbers. In many cases, buyers can purchase fractional points or multiple points depending on pricing options available at the time of rate lock.

For example, you may see options like:

• Zero points with a higher interest rate

• Half a point for a small rate reduction

• One point, two points or three points for deeper rate reductions

Each option comes with its own upfront cost and monthly payment. The goal is to find the balance where the monthly savings justify the upfront expense based on how long you expect to keep the mortgage.

How Point Costs Interact With Other Closing Expenses

It is also important to understand how discount points fit into your overall closing cost picture. Points are paid at closing, just like title fees, escrow items, and prepaid expenses. They do not replace those costs.

For buyers using Down Payment Assistance Programs, this becomes especially important. When assistance is involved, every dollar of upfront cost matters. In these cases, discount points may still be possible, but they need to be evaluated alongside available assistance options, including The Doce Mortgage Group HomeZero Program, which is designed to help qualified Florida buyers minimize upfront cash requirements.

Because of these moving parts, point decisions should never be made in isolation. They should always be reviewed in the context of total cash to close, expected time in the home, and long term affordability.

How Much Can Mortgage Discount Points Lower Your Interest Rate In 2025?

The amount your interest rate drops when you buy mortgage discount points depends on market pricing at the time you lock your rate. In 2025, it is common for one discount point to reduce the interest rate by around one quarter of a percent, although this can vary slightly day to day.

That reduction may sound small at first, but it can have a meaningful impact on both your monthly payment and the total interest paid over time. On larger Florida loan amounts, even small rate changes can add up quickly.

For example, a buyer with a $400,000 mortgage who lowers their rate by a quarter percent could see a monthly payment drop that adds up to many thousands of dollars over several years. The exact savings depend on the loan term and how long you keep the mortgage.

How 2-1 And 3-2-1 Temporary Buydowns Compare To Discount Points

Temporary buydowns, such as 2-1 and 3-2-1 buydowns, reduce the interest rate for the first few years of the mortgage instead of for the full loan term. Unlike mortgage discount points, which permanently lower the rate, temporary buydowns offer short term payment relief during the early years of homeownership.

With a 2-1 buydown, the interest rate is reduced by two percent in the first year and one percent in the second year before returning to the full note rate in year three. A 3-2-1 buydown follows a similar structure, starting three percent lower in the first year, two percent lower in the second year, and one percent lower in the third year.

These buydowns are often funded through seller credits or other negotiated contributions at closing. Instead of paying discount points to permanently lower the rate, the funds are placed into a temporary escrow account that subsidizes the payment during the buydown period.

Temporary buydowns can make sense for Florida buyers who expect their income to increase, anticipate refinancing later, or want lower initial payments while adjusting to homeownership costs. However, unlike discount points, the payment will rise over time, so buyers must be prepared for the full rate once the buydown period ends.

This section sets up a clean contrast before you move into rate variability and pricing mechanics, and it does not disrupt your later break even or refinancing discussions.

Why Interest Rate Reductions Are Not Fixed

It is important to understand that discount points do not come with a guaranteed rate reduction formula. The value of a point changes based on several factors tied to the broader mortgage market.

Key factors that influence how much your rate drops include:

• Overall interest rate trends

• Investor demand for certain loan types

• Your credit profile

• The loan program you are using

Because of this, one buyer may see a slightly larger or smaller rate reduction than another buyer purchasing the same number of points on a different day.

This is why point decisions should always be based on real time pricing, not assumptions from past transactions.

Why Florida Buyers Often See Strong Value From Points

Florida buyers often see stronger value from discount points because of higher average loan amounts. According to recent housing data published by Florida Realtors, median home prices across many Florida metros remain elevated compared to national averages. Larger loan balances magnify the effect of interest rate reductions.

When a quarter percent reduction is applied to a higher balance, the monthly savings increase accordingly. This is one reason long term Florida homeowners often explore point options when rates are in the mid six percent range.

That said, points are still a personal decision. A buyer planning to move in three years may not benefit the same way as someone planning to stay for ten years or longer.

Comparing Rate Options Before You Decide

When reviewing rate options, focus on:

• The upfront cost of each point option

• The monthly payment difference between rates

• How long it would take to recover the upfront cost

If you want help reviewing real pricing options based on your situation, you can request personalized numbers by choosing to Get a Free Quote. Seeing actual figures tied to your credit profile and loan size often makes the decision much clearer.

What Is The Break Even Point When Buying Mortgage Discount Points?

To find the break even point, you compare two numbers:

• The total cost of the discount points paid at closing

• The monthly savings created by the lower interest rate

You then divide the point cost by the monthly savings. The result tells you how many months it takes to recover what you paid upfront.

For example, if you pay $4000 for one discount point and your monthly payment drops by $100, your break even point would be forty months. If you expect to stay in the home longer than that, the savings continue beyond the break even point. If you move or refinance sooner, you may not fully recover the cost.

Why Break Even Timing Matters For Florida Buyers

Florida buyers often face unique timing considerations. Some buyers purchase primary homes with long term plans, while others relocate for work or plan to upgrade within a few years. Florida also sees a high level of refinancing activity when rates shift, which can shorten how long a mortgage is kept.

According to mortgage market data tracked by Freddie Mac, refinancing activity tends to increase quickly when rates drop even modestly. That means buyers who purchase points should always consider the possibility of refinancing before reaching their break even point.

Break even timing matters because discount points only create value if you keep the mortgage long enough to benefit from the lower payment. If you refinance early, the remaining savings disappear even though the upfront cost has already been paid.

How To Estimate Your Break Even Point Accurately

When estimating break even timing, be sure to factor in:

• Your expected time in the home

• The likelihood of refinancing if rates change

• Your comfort level with higher upfront costs

Many buyers find that seeing their personalized numbers makes the decision much easier. If you are at the stage where you want to review actual loan options and timelines, using Our Application portal can help generate accurate figures tied to your situation.

Once you understand your break even point, discount points stop feeling confusing. They become a simple timing decision based on how long you expect to keep your mortgage and how much value you place on lower monthly payments.

Can Seller Credits Be Used To Pay For Mortgage Discount Points In Florida?

Yes, seller credits can often be used to pay for mortgage discount points in Florida, as long as the loan program guidelines allow it. Seller credits are funds the seller agrees to contribute toward the buyer’s closing costs instead of reducing the purchase price.

Discount points are typically considered an eligible closing cost. That means buyers can use seller credits to buy down their interest rate without increasing the amount of cash they bring to closing. This can be especially helpful in higher rate environments, where lowering the rate has a noticeable impact on monthly payments.

Seller credits are negotiated as part of the purchase contract. The amount allowed depends on the loan type and the size of the down payment. Credits can usually be applied toward items like:

• Discount points

• Title and settlement charges

• Prepaid taxes and insurance

Seller credits cannot be applied to the down payment itself. Buyers must also be careful not to exceed program limits, since unused credits are not refunded.

For buyers using Down Payment Assistance Programs, seller credits may still be available, but they must be coordinated carefully. When assistance is involved, options like The Doce Mortgage Group HomeZero Program can also help reduce upfront cash needs while keeping payments affordable.

Do Mortgage Discount Points Work The Same Across All Loan Types?

Mortgage discount points work similarly across most loan types, but there are important differences Florida buyers should understand. Points always represent prepaid interest, but pricing flexibility and overall impact vary by program.

Conventional loans usually offer the most flexibility. Buyers can often choose from several rate options with different point levels, including fractional points. This allows for more control over how much is paid upfront versus how much is saved monthly.

FHA loans also allow discount points, but the overall benefit must be evaluated alongside mortgage insurance costs. Even with points, the insurance component plays a large role in the total monthly payment.

VA loans allow discount points as well. Many VA buyers focus on minimizing upfront costs, but points can still make sense for buyers planning to stay in the home long term, especially when rates are elevated.

Across all loan types, points remain optional. They do not change the loan term or prevent future refinancing. The decision always comes down to timing, expected length of ownership, and how you want to balance upfront costs with monthly savings.

Should You Buy Mortgage Discount Points If You Plan To Refinance?

Discount points usually make more sense when:

• You plan to stay in the home long term

• You do not expect to refinance soon

• Monthly payment stability matters

They tend to be less appealing if your timeline is uncertain or if you are closely watching for rate improvements.

Can Mortgage Discount Points Be Tax Deductible?

Mortgage discount points may be tax deductible in certain situations, but the rules depend on how the loan is structured and how the property is used. For purchases, points are often deductible all at once, while on refinances they are amortized over the life of the loan, rather than all at once.

The IRS generally treats discount points as prepaid interest. This means deductions may be spread out across the life of the loan unless specific conditions are met. Investment properties follow different rules.

Because tax treatment can vary, buyers should always confirm how points apply to their individual situation before assuming any tax benefit.

Common Misunderstandings About Mortgage Discount Points

Many Florida buyers confuse discount points with other mortgage related charges. Clearing up these misunderstandings helps avoid confusion at closing.

Common myths include:

• Points are required fees

• Points are the same as closing costs

• Points always save money

In reality, points are optional, they only impact the interest rate, and they only save money when the mortgage is kept long enough.

FAQ’s

Are mortgage discount points refundable?

No, once paid at closing, discount points are not refunded even if you refinance or sell later.

Can discount points be rolled into the loan amount?

In some cases they can be included in the total loan amount, depending on program guidelines and available equity.

Do first time buyers use discount points?

Yes, many first time buyers consider points, especially when planning to stay in the home long term.

Are discount points available with zero down options?

They can be, but they must fit within program rules and available credits.

How many discount points can you buy?

The number depends on market pricing and program limits, but most buyers consider zero to two points.

How We Help Florida Buyers Decide If Discount Points Make Sense

We know deciding whether to buy mortgage discount points can feel overwhelming. Our job is to help you understand the numbers, the timing, and how each option fits your long term plans. We walk through real scenarios, explain tradeoffs clearly, and help you choose what aligns with your goals.

Our team at The Doce Mortgage Group has been recognized as one of the Best Mortgage Brokers in several cities throughout Florida. That recognition reflects our focus on education, transparency, and results.

We also encourage you to read what other buyers have shared by visiting our customer reviews to see how we support Florida homeowners through every step of the process.

If you want personalized guidance and clear answers, Call us today at 305-900-2012 to discuss whether mortgage discount points are the right move for your Florida home purchase.